It’s hard to believe, but it’s been 12 years since Groupon was launched – and since then, coupon apps have become a growing, vital, and hotly-contested market. In fact, the nine coupon apps we focused on for this story are responsible for a collective 53 million downloads on Android alone.

As the pandemic continues to disrupt brick-and-mortar and online retailing, we at TrueData saw an opportunity to leverage our Big Data and mobile data capabilities to analyze shifting consumer behavior and shopping patterns to help coupon apps capture their share of category growth.

If your coupon app has seen growth under COVID, how much do you know about the customers you have acquired post-COVID? And how can you apply customer and competitor intelligence to claim a greater share-of-wallet from them? Let’s explore.

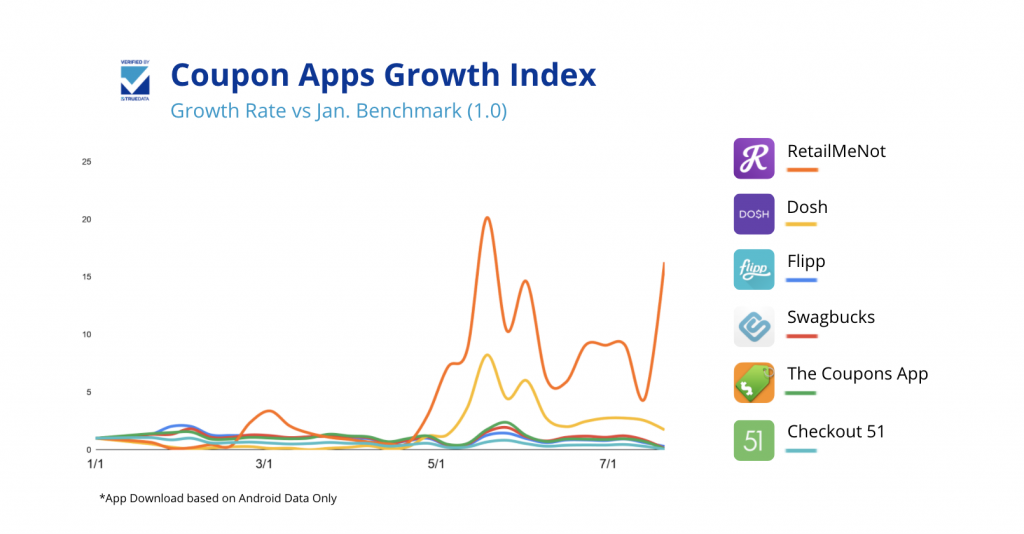

As this graph shows, COVID has had a demonstrable impact on app install velocity for the coupon sector. RetailMeNot and Dosh, in particular, saw download spikes starting in May. One possible reason for RetailMeNot’s steep increase? It offers a dedicated “COVID-19 Savings Hub” page.

Are there gender differences among coupon app users? Yes. While the average ratio of male users is around 25%, more than ⅓ of Swagbucks users and almost 42% of Dosh users are males. If you’re trying to reach male heads of households making purchasing decisions, you may want to explore why and how these apps have attracted more male customers.

Language is another differentiator among coupon app users. As the graph below shows, Flipp is the clear leader among Spanish speakers, who represent more than a quarter of its user population. That’s double the percentage of its closest competitor, Coupons.com. U.S. Spanish speakers have an immense amount of purchasing power. Flipp has been able to find growth by more effectively reaching and acquiring this vital consumer sector.

Coupon apps are primarily used by older people, with adults aged 35 and up comprising the vast majority of users for all major coupon apps. Among older users, Rakuten is #1 with more than ⅓ of its users over the age of 55. Younger deal seekers on the other hand have a preference for mobile-first apps, such as Dosh and Swagbucks. This may be because Dosh focuses on cash back at local spots (which may appeal more to socially active young people) and Swagbucks offers cash-strapped younger users rewards for activities such as taking surveys and playing games.

The key to organic growth is to build loyalty among your existing users. That’s a challenge in the competitive world of coupons because people who love coupons are likely to seek more that one app to fulfill their hunger for deals. For coupon app companies, it’s helpful to know who else your users are frequenting for coupons and cash-back offers. This can help you determine which competitive targets to take on to increase your share-of-wallet.

For example, the graph below shows that nearly half of Krazy Coupon Lady’s users and a third of Flipp’s users also use The Coupons App.

It is strategically important for an app like Krazy Coupon Lady to know that its primary competitors are The Coupons App, Coupons.com, and Checkout 51.

When you know what other apps your users tend to download – beyond your competitive set – you can gain valuable insights to help drive your growth plans. For example, the app ownership index below provides insights into retail apps that Flipp and RetailMeNot users over-index for. It shows that Flipp users are 26 times more likely to shop at ALDI, while RetailMeNot users are 21 times more likely to shop at Old Navy. This gives apps like Flipp the information they need to offer coupons or deals they know their users are more likely to want – thereby helping them to acquire customers or increase ARPU.

Not all coupons are redeemed online; many are used at retail outlets still open during the pandemic. Our location visitation data overlaid on top of app ownership data can help guide any mobile app to physical retailers where their customers already shop. For example, as the graph below shows, 19.4% of recent Lowe’s store visitors have also downloaded the Groupon app. It’s no surprise, then, that a recent check of the Groupon site showed a total of 32 Lowe’s offers.

Mapping out overlaps is helpful, but it may not give you a relative sense of importance. That is where an index can be very helpful as it establishes a ratio between average behavior and the behavior of a specific cohort. Here we have indexed retail visitation data to a Lowe’s or Best Buy store against app ownership. As it turns out, recent Lowe’s store visitors have an affinity for Fetch rewards – they are 26 times more likely than the average person to have the Fetch rewards app. Best Buy store shoppers, on the other hand, have a stronger affinity for Dosh, The Coupons App, and Rakuten.

As in many mobile categories, coupon app downloads have surged during the pandemic. With accurate, detailed demographic, POI, and app ownership data – and the analytical tools to exploit them – mobile app publishers can take advantage of untapped opportunities to increase downloads and drive app usage. Contact us to see how our ML platform can help you drive better growth for your mobile business.

Subscribe For Updates